Owning your own home: a step-by-step guide to obtaining a loan

Do you finally have your sights on the ideal property? Here’s what you need to know in order to get the right loan – and how to find a good renewal mortgage.

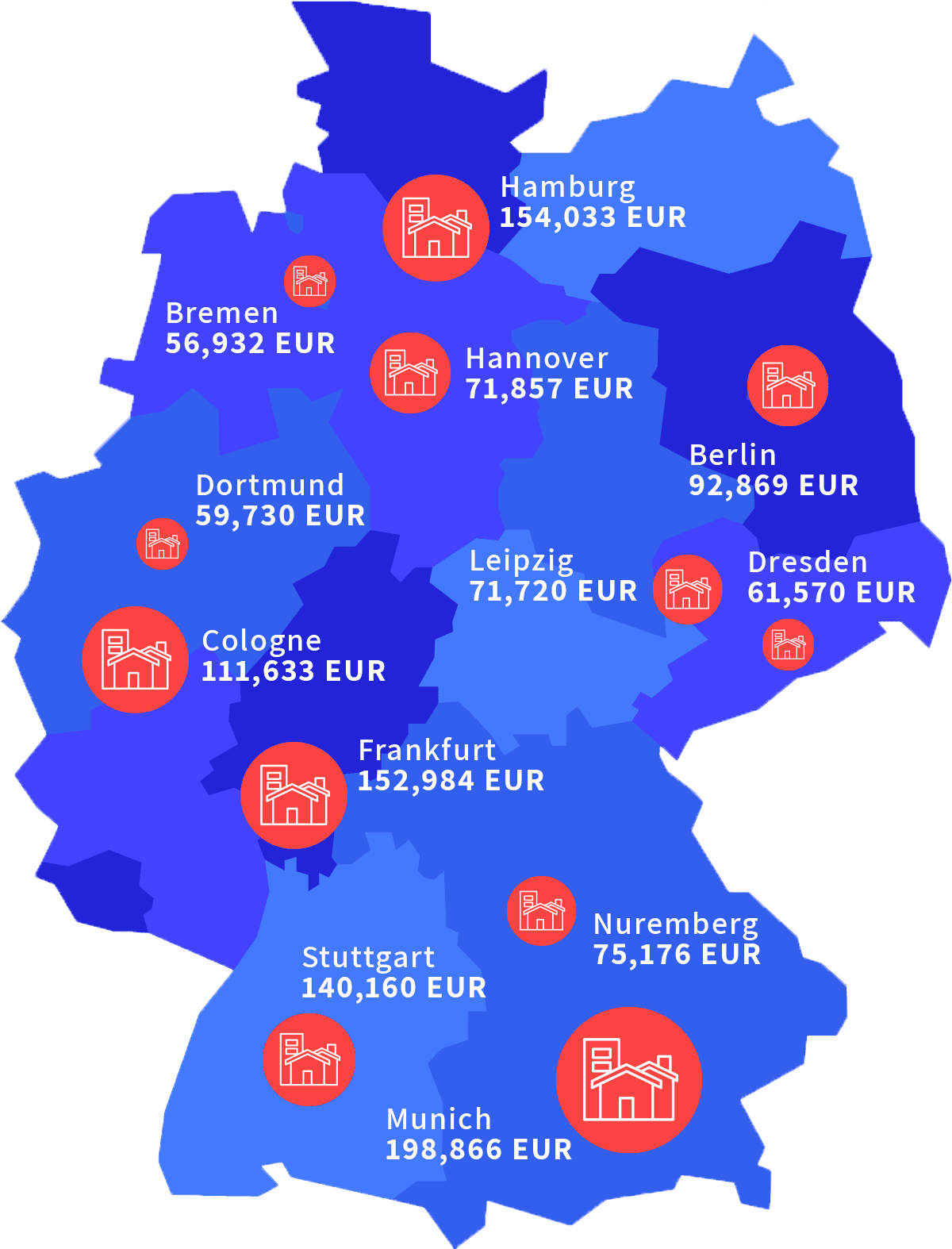

When the dream of owning your own home becomes a reality, the focus shifts to solid financing. This is because most people need to take out a loan in order to close the gap between the amount they have available for a down payment (see the comparative map of Germany) and their remaining needs. In doing so, certain formalities also need to be observed. Key aspects at a glance:

Basis for financing a new development property.

Peaks in the north and the south: In Germany, the average down payment is EUR 93,847.

Source: Interhyp

1. What the bank wants to know.

Before the bank will grant a loan, a property buyer needs to submit, in particular, the following documents:

- A signed loan application.

- A copy of wage and salary statements for the past three months; if a couple is applying and both individuals work, then both need to submit copies.

- Income tax returns for the past two years. Important: Submit all pages, not just the first one.

- Proof of funds available for the down payment, such as a statement for a call-money or term-deposit account.

- Other income: e.g. proof of any capital or rental income.

Property documents, such as site plan, floor plan, land register extracts, any cost estimates for needed renovation/modernisation work.

2. What the law requires.

Since the implementation of the EU Directive on Residential Property Loans in Germany (EU-Wohnimmobilienkreditrichtlinie), stricter standards apply to the awarding of property loans. Banks and other lenders now have to verify the creditworthiness of their customers more precisely. For instance, it has to be ensured that a borrower is capable of fully repaying the loan over a realistic period of time, such as prior to retiring. The aim of the new directive is to protect consumers against ill-considered and poorly planned loans with monthly payments that are too high. “Today, more than ever, it is important to make a long-term, realistic assessment of the customer’s overall financial situation. At MLP, this has always been the standard – and the basis for every loan,” says Marc-Philipp Unger, head of property and financing at MLP.

3. What else is important.

The purchase or construction of a property is often the largest financial challenge in life. Therefore, no one should act rashly simply because interest rates are currently still so low. More than ever, a property’s location and condition are the decisive quality criteria in making the selection. Moreover, the essential precondition for any loan is that the borrower has regular income and, ideally, a sufficient down payment as the basis for the purchase of the home, so that initial one-time expenses are covered (such as notary fees, land register costs, and land transfer taxes). In this way, solid financing is possible without placing significant limitations on the current standard of living.

4. Finding the right mortgage renewal.

Is the term of the loan you used to finance your property about to expire? Here’s how you can find good follow-on financing:

- Ideally 12 to 24 months before the end of the interest rate lock-in period, start comparing offers. Note: Your current lender has to make you an offer at least three months before the end of the interest rate lock-in.

- In addition to the effective interest rate, important criteria for the decision include the ability to make unscheduled repayments and to change the rate of repayment. For example, if your income increases or your investments become due for repayment, it’s possible to pay down your debt more quickly.

- Important when switching to another lender: Calculate whether the amount of interest you’ll save is more than the costs for reassigning and reconveying the collateral in the land register. Tip: Some banks do no charge any refinancing fees. MLP advisors can also provide specific assistance here as well.

- Also for new loans, remember: choose the longest possible interest rate lock-in – 10, 15, or even 20 years, depending on the amount of the outstanding loan. That enables planning certainty.

Regardless of whether you’re looking for a home-purchase loan, a home-construction loan, or follow-on financing, your MLP advisor can assist you at every stage of the process and answer all of your questions. Other useful checklists for property financing are available here.

Contact us now or check your mortgage options with our Mortgage Calculator