How can I secure favourable interest rates for real estate financing?

Anyone who is currently looking for a property and needs the corresponding financing will have been sobered to discover that interest rates have almost tripled compared to January 2022.

A large proportion of prospective buyers therefore hardly have the chance to buy a flat or a house any more; the monthly burden for interest and repayment is simply too high. In many cases, the comparison between buying and renting is no longer in favour of buying a property. In addition, property owners who have taken out financing in the last five years must expect follow-up financing that will be far more expensive than the favourable interest rate from the past.

Is there a means to respond to these two scenarios? Yes, it is possible.

A financing instrument that is hardly in demand anymore in times of low interest rates has awakened from its slumber. The building savings contract.

What kind of instrument is it, how does it work and how can it contribute to problem solving?

History of building savings contract:

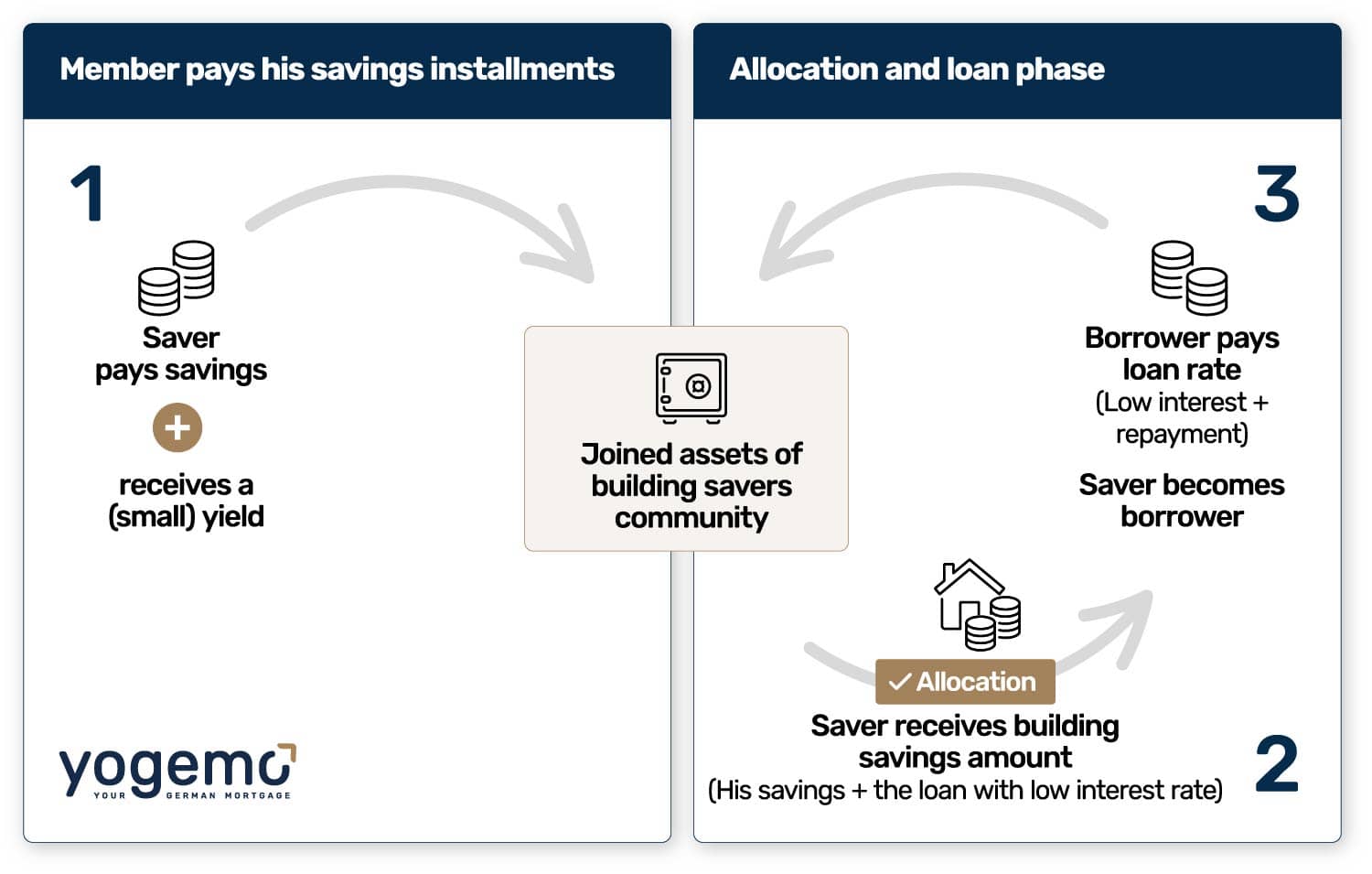

- Since the beginning of the last century, the building savings contract has been the instrument for saving and financing a home in Germany. The main objective of this financial instrument was to secure low interest rates for the future and thus to know the exact credit rate for the loan already in the savings phase. For this, an equally comparatively low interest rate is accepted in the savings phase.

- Building savings banks are a community of like-minded people. The capital of the savers serves the buyers as a loan with very low interest rates.

- In simple terms, you save a monthly credit balance over a few years and then have the right to use this credit balance and a loan with a fixed interest rate for a purchase, modernisation or follow-up financing. The loan should then also be repaid in a relatively short time.

- From this basic principle, building societies have created a universe of a variety of products with different flexibilities, maturities, savings, credit and loan interest rates.

In a nutshell, you can already secure a loan interest rate of 1.25% for the future. A loan can be drawn down in as little as 3 – 5 years.

If you do not need a loan, the saved capital is available at any time. A building savings contract can also be given to the children as a gift. German grandparents and parents have already taken out these contracts for their grandchildren and children. It is a great way to provide for the future.

Your-German-Mortgage has developed interesting concepts for its expat clients together with a large German building society. Financing of up to 100% of the purchase price of a property is possible with a good credit rating. Also for Blue Card holders and also in combination with a classic loan.